2024 ended the year with continued outperformance by the S&P 500, marking the first instance of back-to-back years of 20%+ returns since 1998/1999. The first quarter of 2025 has told a different story as investor sentiment has waned. Risk-off sentiment has been driven by concerns around macro softening and punctuated by volatile trade tariff headlines.

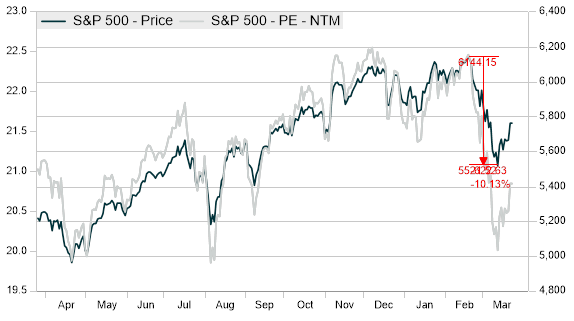

It was not surprising to see enhanced volatility in the first quarter- years of outsized gains left equity valuations stretched with the S&P 500 seeing a large portion of earnings growth and returns driven by extremely narrow leadership. The S&P 500 entered the year with a Forward 12 Months Price/Earnings multiple of 21.5x, compared to a 10-year average of about 18x.

As market participants delt with uncertainty from a variety of sources, valuations contracted with the S&P 500 temporarily dipping into correction territory on March 13th after falling more than 10% from the February 19th highs.

Perhaps what’s been more interesting has been the churn under the surface- there has been pronounced rotation within segments of the equity markets. Market rotations take various shapes and forms but are ultimately driven by shifts in investor preference across asset classes, geographies, and sectors.

The beginning of a rotation is often inspired by valuation discrepancies, when investors shift assets to areas of the market they perceive as being undervalued, with those funds sourced from assets they believe to be overvalued. Differences in valuation ebb and flow, but as relative valuations become further and further stretched compared to historical averages, the more likely it becomes for a rotation to occur. Discrepancies in valuation are just one piece to a complex puzzle- other factors like stage of the economic cycle, changes in interest rate policies from central banks globally, risk appetite, and heightened uncertainty play a role in both the magnitude and duration of the rotation.

Three of the more notable rotations under way in 2025 include a rotation away from growth stocks and the Magnificent 7, a shift toward relatively more value-oriented international stocks, and significant sector rotation.

- Magnificent 7 becomes a source of funds after long-term, dizzying outperformance:

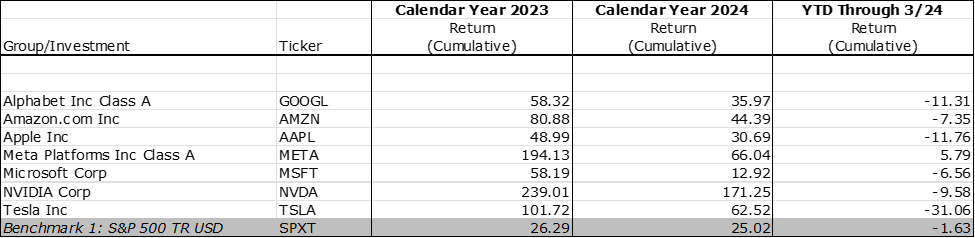

Last year, the Magnificent 7 stocks accounted for more than half of the S&P 500’s 25.0% total return. As of the end of 2024, the Magnificent 7 stocks collectively traded at a Forward 12 Months Price/Earnings ratio of about 31x – a premium of almost ten “turns” compared to the S&P 500’s 21.5x multiple and a premium of exactly double the 15.5x multiple of the equal weighted S&P 500.

The rotation away from the Magnificent 7 stocks is certainly related to concerns about valuation, but it is worth pointing out that, due to the law of large numbers, it becomes increasingly difficult to sustain the high earnings and margin growth rates experienced in prior years. Surely, these stocks have earned the right to command a premium multiple when compared to the broader index as some of the most innovative constituents. However, as sentiment fades in the face of an uncertain economic backdrop and forward growth rates begin to look ambitious, investors have a hard time rationalizing sky-high multiples. As positioning unwinds, 6 of the 7 names have moved lower and experienced multiple contraction, leaving the group collectively trading at about 26x forward earnings.

2. Non-U.S. markets have seen significant rotation in their favor:

Coming into the year, the MSCI All Country World Index ex-U.S. traded at a 40% discount to U.S. equities when measured by Forward 12 Months Price/Earnings multiples (compared to a 10-year average discount of 24%). Again, relative valuation has inspired rotation, but other factors are at play.

Non-U.S. markets have been helped by a rotation away from growth stocks in favor of value, but also by currency tailwinds as the dollar has substantially weakened in major currency pairs including EUR, GBP, and JPY. European indices have been boosted by massive defense and government spending plans from Germany and other members of the European Union. So too, have Asian markets benefited from developments from Chinese artificial intelligence including DeepSeek’s models, with some indicating that AI is more of a commodity than previously thought.

The magnitude of outperformance due to the rotation from U.S. into international stocks is small in the context of the last decade, even at 10%+ year-to-date. Strategists remain split on whether the rotation will continue after long-term underperformance from international equities.

3. Sector rotation:

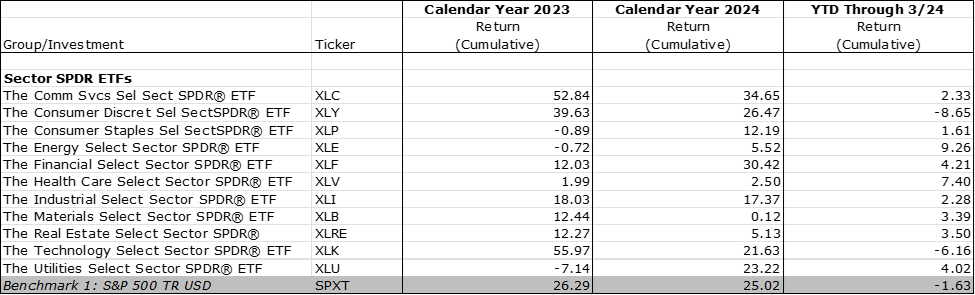

During periods of sustained economic growth and expansion, investors favor cyclical sectors like technology and consumer discretionary. As sentiment sours, funds flow into more defensive sectors like healthcare and consumer staples, which are less sensitive to economic cycles.

2025 has seen some of 2024’s laggards find renewed investor interest and have emerged as new leaders. Basic materials, healthcare, and energy having been underperformers in 2023 and 2024 have become leaders year-to-date. Conversely, technology and communications services have seen their fortunes reverse, now the worst performing sectors year-to-date.

How far these rotations can continue has analysts divided. Markets have seen pull-backs in mega-cap tech stocks as international stocks and small caps emerged as leaders, only to see renewed enthusiasm for artificial intelligence and a seemingly unquenchable desire for exposure to innovation and momentum. One thing is certain- when rotations occur and market leaders become laggards, we are reminded of the importance and value of remaining disciplined in diversification.